- LOGIN

- MemberShip

- 2026-05-05 16:52:45

- Policy

- Reimb standards set for biliary tract cancer drug Pemazyre

- by Lee, Tak-Sun Aug 30, 2024 05:50am

- Pemazyre (pemigatinib), a targeted therapy for biliary tract cancer supplied to Korea by Handok, has successfully received reimbursement standards from the Health Insurance Review and Assessment Service's Cancer Disease Review Committee (CDDC). The reimbursement standards for the immuno-oncology drug Tevimbra were also set at the meeting. Merck's Erbitux has been granted an extended reimbursement. The CDDC held a meeting on the 28th to review reimbursement for new anti-cancer drugs and extend reimbursement for listed drugs. As a result, Handok’s Pemazyre may be reimbursed for the treatment of adults with previously treated, unresectable locally advanced or metastatic cholangiocarcinoma with a fibroblast growth factor receptor 2 (FGFR2) fusion or other rearrangement. Also, Tevimbra may be reimbursed as monotherapy in adult patients with unresectable, recurrent, locally advanced, or metastatic esophageal squamous cell carcinoma who are unable to continue prior platinum-based chemotherapy or who have relapsed or progressed after receiving prior therapy. In the case of Erbitux, which is primarily used to treat colorectal cancer, the application to extend its reimbursement as combination therapy with encorafenib (with bi-weekly Erbitux) as a treatment for adult patients with previously treated metastatic colorectal cancer with a confirmed BRAF V600E mutation was approved by CDDC. On the other hand, MSD Korea's rare disease drug ‘Welireg Tab’ failed to set reimbursement standards. In addition, Ipsen Korea's ‘Cabometyx Tab,’ Ono Pharmaceutical Korea’s ‘Opdivo Inj,’ and drugs containing anastrozole and letrozole also failed to establish reimbursement standards. In addition, the CDDC reviewed the use of prophylactic G-CSF for dose-dense MVAC/CMV therapy for urothelial cancer, TIP therapy for testicular cancer, and cabazitaxel therapy for prostate cancer with drugs such as Neulasta, reflecting the opinions of the medical community, but decided to maintain the current state.

- Company

- API competition↑ with entry of Chinese and Indian pharmas

- by Son, Hyung-Min Aug 30, 2024 05:50am

- Chinese and Indian companies developing active pharmaceutical ingredients (APIs) are accelerating their entry into Korea. Numerous Chinese and Indian companies as well as domestic companies participated in 'CPHI Korea 2024,' an exhibition for the global pharmaceutical, bio, and health functional food industry that was held at COEX in Samseong-dong, Seoul for 3 days from the 27th, to promote their API development capabilities. Domestic companies also participated in the event to showcase their technology. Domestic API companies highlighted the quality of their products as a strategy to differentiate themselves from overseas companies. A large number of Chinese and Indian API companies participate in CPHI China was the largest participating country at CPHI Korea 2024. More than 140 Chinese pharma and biotech companies participated in the event, which accounted for almost half of the 340 exhibitors. (Clockwise from the top left) Jiangxi Synergy, Bloomage Biotechnology, Zhejiang Biosan, Hubei Honch Pharmaceutical, Xieli Pharmaceutical from China As China supplies nearly half of the world's APIs, these companies are highly influential in the API market. Korea also imports the largest amount of APIs from China. These companies plan to actively target the domestic market to further increase their influence in Korea. China has been turning its eye to markets outside the U.S. after the U.S. strengthened sanctions against China. The U.S. has been implementing biosecurity legislation that would ban Chinese biotech companies from doing business with the U.S., favoring its own biotech companies. In response, Chinese companies have been eyeing the Korean market, which was why many Chinese companies participated in BIO KOREA 2024 in May to promote their company and technologies. The second largest overseas participant after China was India. India owns the second-largest API market following China. India accounts for 20% of the world's supply of APIs. India's pharmaceutical industry has been growing rapidly, focusing on biopharmaceuticals and contract development manufacturing organizations (From the left) Krishna Enzytech, Ashwagandha, Anupam Rasayan, Oceanic Pharmachem from India Various API, health functional food, and additive developers such as Krishna Enzytech, KSM-66 Ashwagandha, Anupam Rasayan, and Oceanic Pharmachem attended the event. In particular, the health functional food company Ashwagandha, participated as a title sponsor of the event. Korean API companies, including Novarex and Samoh Pharm participated at the event..."secured competitivity with quality" Many domestic companies also participated in CPHI Korea 2024. The second largest amount of companies that participated in the event were Korean companies, following China. Kukjeon Pharmaceutical, Samoh Pharm, Inist ST, Seoheung, and Novarex, among others, promoted their technologies for developing various APIs. (Clockwise from top left) Inist ST, Rihu Healthcare, Samoh Pharm, Suheung from Korea Domestic companies expressed high hopes based on the quality of their products. Currently, China and India dominate the global API market. Korea also imports most of its APIs from these countries. The problem is that domestic synthetic drugs are significantly less competitive in price than their Chinese and Indian counterparts, and the high dependence on overseas APIs limits the opportunities for domestic companies. “It is virtually impossible to keep up with China and India in terms of price competitiveness,” said an official from a domestic API company. “Domestic companies need to differentiate themselves in quality through superior manufacturing facilities and quality development capabilities to stand a chance.” However, the government's support is urgently needed to overcome the price competitiveness of overseas companies, and the industry's opinion is that no significant policies have been implemented up to now. The government's policy direction seeks to advance the self-sufficiency rate of APIs for pharmaceuticals, but the policies have not shown a significant impact until now. In particular, there has been a history of disruptions in the production of essential medicines due to difficulties in the supply of raw materials, including the deployment of THAAD, the valsartan crisis, COVID-19, and trade wars, but even after the pandemic turned endemic, the self-sufficiency rate of APIs has not improved. According to the Ministry of Food and Drug Safety, 31 of the 567 finished drugs reported to have been suspended from production, import, and supply from 2017 to June 2022 due to problems in the supply of APIs. 17 of these were national essential medicines. “To compete not only with the U.S. and Europe, but also with China, India, and Southeast Asia, that own prices competitivity, we need support policies at the finished drug level,” said an official from another domestic API company. ”The government has not clearly presented measures to support for self-sufficiency of APIs in Korea. The goal should not be to maintain a certain level of self-sufficiency, but to support the domestic pharmaceutical industry to compete with the global market.”

- Company

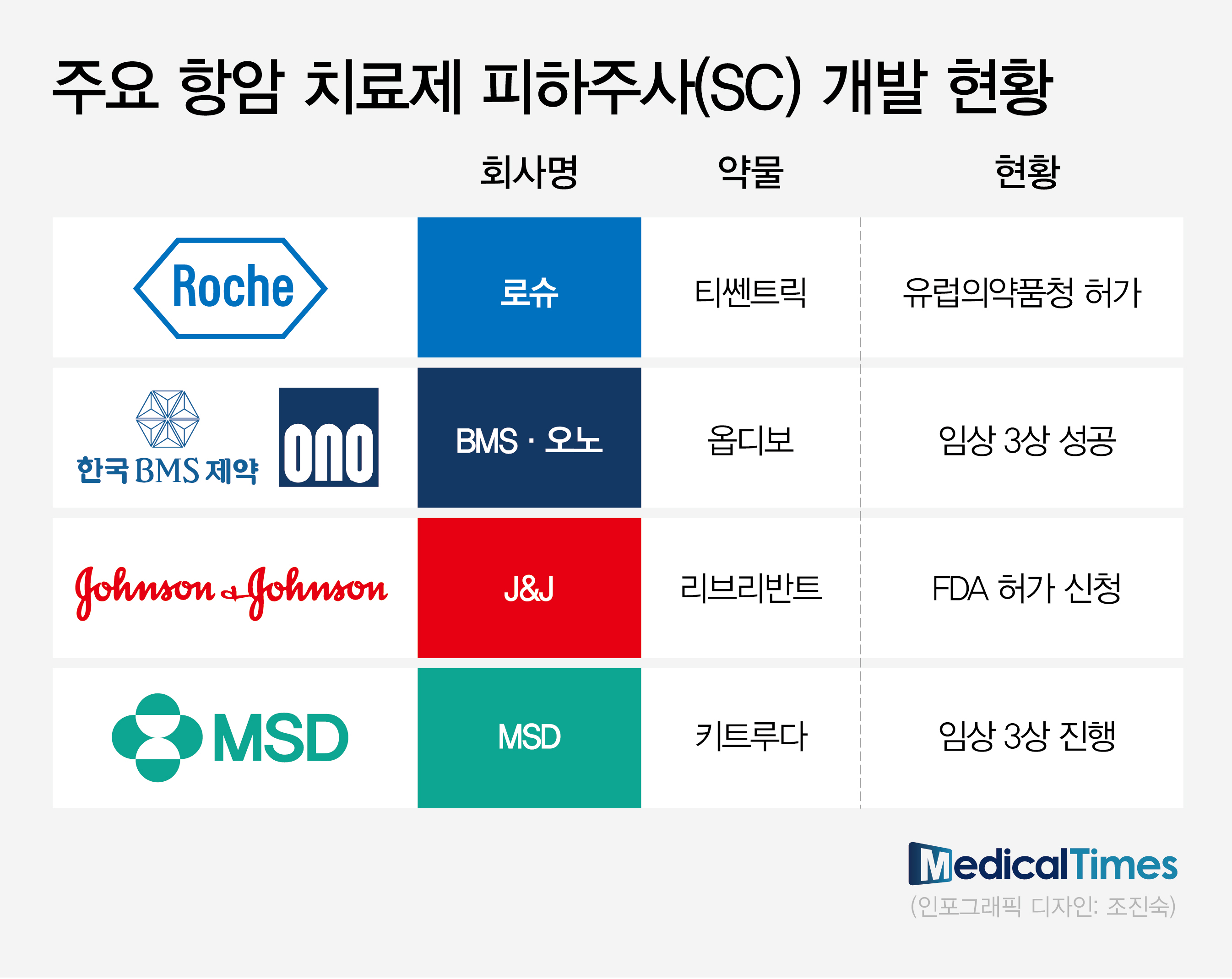

- Anti-cancer drug trends changes from IV→SC

- by Moon, sung-ho Aug 30, 2024 05:50am

- Global pharmaceutical companies speed up the development of subcutaneous (SC) formulations of their proprietary intravenous (IV) medications. To overcome the disadvantage of IV formulation medications that have long administration duration, more anti-cancer drugs are shifting to SC formulations. Following the trend, Korean companies with SC formulation technology are gaining attention. Then, what can we predict about the success in real-world clinical practices? While the shift to SC formulation of anti-cancer drugs is trending, pharmaceutical‧biotech industries focus on real-world clinical practices. Global pharmaceutical companies with IV formulations of anti-cancer drugs are proactively conducting clinical trials to transition to SC formulation products. (Table) RocheAccording to pharmaceutical and biotech companies on August 24th, global pharmaceutical companies with proprietary IV formulations of anti-cancer drugs are proactively conducting clinical trials to transition to SC formulation products. SC formulation products are injected into the subcutaneous layer of the skin. Injection sites are typically arms, thighs, and abdominal region. Until now, anti-cancer drugs were available primarily as IV formulations, which inject medications into veins. IV formulation has the advantages of fast absorption and accurate administration but has the disadvantage of taking a long time. For IV injection of anti-cancer drugs, patients were burdened by having to visit hospitals and withstand four to five hours of needle insertion. In contrast, developing anti-cancer drugs as SC formulations has the advantage of substantially improving patient convenience of administration. The administration duration was reduced from a couple of hours to a maximum of ten minutes. Therefore, patients do not need to stay in the hospital for a long time for anti-cancer drugs. As a result, global pharmaceutical companies with immune checkpoint inhibitors are proactively conducting clinical trials and applying for approvals to transition to SC formulations. Following Roche's 'Tecentriq (atezolizumab)' SC obtaining marketing authorization from the European Medicines Agency (EMA) in January, BMS and Ono Pharmaceutical's R&D of 'Opdivo (nivolumab)' and 'Rybrevant (amivantamab)' is nearing the end. These immune checkpoint inhibitors share the same goal to defend against their sales decrease due to patent expiration. Furthermore, the development of SC formulation products has gained more attention since SC formulations have a greater advantage in patient access in the global market, especially in the U.S. market. Recently, J&J confirmed the non-inferiority of SC formulations compared to IV formulations through the Phase 3 PALOMA-3 study, presented at the American Society of Clinical Oncology (ASCO) meeting. Based on the results, J&J has recently applied for additional U.S. FDA approval on Rybrevant SC formulation. Professor Byoung Chul Cho (Director of the Lung Cancer Center at Yonsei Cancer Hospital) said, "The United States provides incentives to using injections, and the amount of incentives is the same between IV injectable or SC injectable," and explained, "There is no need to maintain IV formulation injectables, which commonly induce injection-associated adverse reactions." Professor Sun Min Lim (Division of Medical Oncology, Department of Internal Medicine, Yonsei Cancer Hospital) also said, "SC injectables only take 1-2 minutes for Rybrevant administration. The common adverse reactions of IV injectables are fever and lowered blood pressure," and added, "In my opinion, SC injectables can reduce such adverse reactions." In the global market trend, clinical practices in South Korea are accelerating the introduction of SC formulation products, which overcome the previous disadvantages of IV formulation. For example, Roche's Phesgo has been recently introduced with reimbursement. Phesgo is an anti-cancer drug developed by changing the IV formulations of Herceptin (trastuzumab) and Perjeta (pertuzumab) to SC formulations. It received approval in September 2021 as the first investigational biopharmaceutical. Phesgo was developed by combining two IV formulation products into SC formulation. It is known to decrease the administration duration for patients with breast cancer substantially. It has been designated as an innovative new drug (IND) and is reimbursable, leading to its recent use in clinical practices. If patients with metastatic HER2-positive breast cancer who have been receiving the maintenance therapy, IV formulations of Herceptin plus Perjeta every three weeks, were to change to Phesgo SC, administration and monitoring duration is expected to decrease from over four hours to 20 minutes. The remaining step is whether the SC formulation can be used in clinical practices in South Korea. While there are clear advantages in patient administration, there are opinions that, unlike in the global market, such as the U.S., it is challenging to quickly replace the existing market in South Korea due to geographic accessibility. Additionally, many believe it will be challenging for healthcare professionals to readily switch to the SC formulation, which they have yet to experience. However, some argue that the fact that most cancer drug administrations are carried out primarily in large hospitals and are performed in the same way in injection rooms is more positive. The large number of patients who can receive treatment may facilitate the rapid establishment of the SC formulation. Professor Park Yeon Hee (Division of Hematolology-Oncology at Samsung Medical Center) said, "Korean patients tend to wait in the hospital, and there are long waits in large hospitals. Therefore, patients may prefer switching to SC formulations," and stated, "In clinical practices, patients may prefer IV injection despite the wait as SC prescriptions, other than clinical studies, have only been made recently."

- Company

- K-bio jumps into developing new drugs for pancreatic cancer

- by Son, Hyung-Min Aug 30, 2024 05:50am

- Korean pharmaceutical and biotech companies have jumped into the development of new drugs for pancreatic cancer, which is categorized as refractory cancer. Prestige Biopharma, New Cancer Cure Bio (NCC-Bio), LigaChem Biosciences, and Aptamer Sciences are conducting clinical trials to challenge the field. These companies plan to investigate the commercialization potential of their candidates through antibody-drug conjugates (ADCs), targeted anti-cancer agents, and new antibody drugs. New ADC drugs target TROP2 for treating pancreatic cancer According to industry sources on August 29th, Aptamer Sciences applied for a patent for its 'Aptamer-Drug Conjugate (ApDC)' and commenced treatment development. ApDC is a next-generation ADC new drug development platform with its proprietary branched linker-payload technology. Pancreatic cancer is known to have the lowest survival rate among cancer disorders. The five-year survival rate of pancreatic cancer is merely 15.9% from 2017 to 2021, according to the National Cancer Center. The early detection rate of pancreatic cancer is less than 10% due to the location of the organ, and the cancer readily metastasizes to peripheral organs. Until now, several domestic and global companies have jumped into developing new drugs for pancreatic cancer but mainly failed in clinical trials. Aptamer Sciences and latecomer companies plan to develop new drugs for pancreatic cancer using their new drug candidates, such as ADC. Aptamer Sciences derived 'AST-203' using the ApDC platform. AST-203 is made by conjugating TROP2-targeting antibody with 'MMAE,' a microtubule disruption agent, with linker 'VC-PAB.' TROP2 is an intracellular calcium signal transducer that regulates cell proliferation and survival. Although this protein is found in healthy cells, it is often overexpressed in cancer cells and is associated with drug resistance. The only TROP2-targeting new drug available in the market is Gilead Sciences' ADC Trodelvy, which is approved for treating triple-negative breast cancer. TROP2 is commonly found in breast cancer, non-small cell lung cancer (NSCLC), colorectal cancer, and pancreatic cancer. The clinical trials for latecomer agents are being conducted to target major solid cancers. In pre-clinical trials, Aptamer Sciences has confirmed the potential of AST-203 in a tumor spheroid model (3D cell culture of spheroids). According to the company, AST-203 showed a 6.7-fold higher tumor penetration rate than an existing therapy, Trodelvy. Additionally, in a pancreatic cancer animal model, AST-203 demonstrated dose-dependent tumor growth suppressive effects and tumor regression, reducing tumor sizes in all experimental animal groups. Aptamer Sciences aims to commence a clinical trial for AST-203 in two years. LigaChem Biosciences (hereafter referred to as LigaChem Bio) is developing TROP2-targeting ADC LCB84. Last year, LigaChem Bio successfully signed a deal with Janssen, a subsidiary of U.S.-based Johnson & Johnson (J&J) to license-out its LCB84. LCB85 consists of LigaChem Bio's proprietary ConjuAll linker and four MMAE, a microtubule disruption agent. ADC consists of a linker, payload (drug conjugate), and antibody. The ConjuAll linker is known to overcome the issue of releasing cytotoxic drugs into the blood and attacking healthy cells. In preclinical studies, LCB84 demonstrated effects in solid tumors not responding to topoisomerase enzymes-based TROP2 ADC payloads. Major ADCs like Enhertu (trastuzumab deruxtecan) incorporate the technology of topoisomerase enzymes. LigaChem Bio received Investigational New Drug (IND) approval from the U.S. Food and Drug Administration (FDA) in June, and the company is currently conducting Phase1/2 studies in the United States. In clinical trials, LigaChem Bio plans to investigate the preventive efficacy of LCB84 monotherapy and the combination therapy of LCB84 plus immune checkpoint inhibitor. Prestige Biopharma·NCC-Bio successfully enter clinical trials In addition to ADCs, various new drug candidates are being investigated for potential treatment of pancreatic cancer. Prestige Biopharma is developing a new antibody drug candidate, PBP1510. PBP1510 works by neutralizing pancreatic adenocarcinoma upregulated factor (PAUF), a protein target for the treatment of pancreatic cancer. The PBP1510 Phase 1/2a trials are being conducted in Spain, the United States, Singapore, and Australia. Through the trials, Prestige Biopharma plans to investigate the safety and tolerability of PBP1510 plus gemcitabine combination therapy. Prestige Biopharma aims to expand PBP1510's indication to ovarian cancer and prostate cancer in addition to pancreatic cancer. PAUF is known to be associated with ovarian cancer and prostate cancer. NCC-Bio will commence the development of a new drug for treating pancreatic cancer using 'KN510713,' a targeted anti-cancer agent and fatty acid oxidation (FAO) inhibitor. The company is conducting clinical trials after receiving approval for the KN510713 Phase 1 trial last year. NCC-Bio, founded by Kim Soo Youl, who used to work at the National Cancer Center, is a biotech company specializing in developing new anti-cancer drugs. KN510713 is being developed as an anti-cancer drug candidate that inhibits catabolism. Its clinical trial is the first anti-cancer agent trial to target inhibiting fatty acid oxidation (FAO) metabolism in cancer. KN510713 works by decreasing cancer cell growth by blocking the energy supply to tumor cells without affecting healthy ones. NCC-Bio is studying the last cohort of the Phase 1 trial and plans to enter the Phase 2 trial next year.

- Policy

- Prices of Dukarb, Rosuzet cut 3 yrs through PVA

- by Lee, Tak-Sun Aug 30, 2024 05:49am

- The insurance ceiling price of 6 drugs has been cut for 3 consecutive years through the price-volume agreement ‘Type C’ negotiations. According to the industry on the 28th, 6 drugs, including Boryung Pharmaceutical’s 'Dukarb', Dong-A ST 'Growtropin II Inj’, Hanmi Pharmaceutical’s 'Rosuzet Tab', Janssen Korea’s 'Concerta Oros ER Tab’, Boehringer Ingelheim ‘Jardiance Duo Tab', and Daewoong Bio’s ‘Gliatamin’, have had their insurance price ceiling lowered for 3 consecutive years from 2022 to 2024 through the price-volume agreement Type C negotiations. In this year's Type C negotiations, the prices of Boryung’s four Dukarb Tab items, which are combination antihypertensive drugs, were cut by -1.0% to -0.6%. In the case of Dukarb Tab 30/10mg, the ceiling price had been KRW 715 in June 2022 but will become KRW 686 from the first of next month. The company’s revenue from Dukarb has also increased significantly. Based on UBIST, outpatient prescriptions of Dukarb Tab rose from KRW 40.5 billion in 2021 to KRW 54.3 billion last year. Growth hormone drug Growtropin II Inj is another case where sales have increased significantly in recent years. Based on IQVIA, its sales increased from KRW 36.7 billion in 2021 to KRW 69.8 billion in 2023. five Growtropin II Inj items received a -5.0% to 0% reduction in their insurance ceiling price. (Source: IQVIA (Growtropin II Inj only), UBIST for the rest) Hanmi Pharmaceutical's four Rosuzet Tab items, a combination drug for hyperlipidemia, received a -1.5% to -1.3% reduction in their insurance ceiling price. The outpatient prescription of Rosuzet Tab (UBIST) also surged from KRW127.8 billion in 2021 to KRW178.8 billion in 2023. (Source: IQVIA (Growtropin II Inj only), UBIST for the rest) Janssen Korea's ADHD drug Concerta Oros ER Tab also received a reduction in their insurance ceiling price for the third consecutive year through PVA negotiations. This time, four of its items received a high rate of price reduction from -5.3% to -5.0%. The drug also showed strong growth in outpatient prescriptions from KRW 15.1 billion in 2021 to KRW 22.8 billion last year (UBIST). The insurance price ceiling of six Jardiance Duo Tab items, which is a combination used for diabetes, was reduced by -4.1% to -3.9%. The drug recorded a high growth rate, from KRW 24.1 billion in 2021 to KRW 39.4 billion in 2023 in outpatient prescriptions (UBIST). Sales of Gliatamin, a brain function enhancer, have continued to soar despite the reimbursement cut and clinical re-evaluations. Outpatient prescriptions increased from KRW 114.3 billion in 2021 to KRW 154.5 billion last year (UBIST). The price ceiling of Gliatamin Soft Cap and GliataminTab received a reduction of -3.3% this time (UBIST). In the case of Gliatamin Soft Cap, the price was KRW 504 per tablet on January 1, 2022, but will drop to KRW 476 next month. Over a three-year period, the reductions made in the insurance price ceiling amounted to -5.6%. On the other hand, starting this year, the National Health Insurance Service will reduce the reduction rate in the reference formula by 30% for innovative pharmaceutical companies or companies with an R&D ratio of more than 10% for drugs that have been subject to PVA negotiations 3 times in 5 years. This year, 17 items received a 30% reduction.

- Opinion

- [Reporter's View] pros and cons of concurrent reimb listing

- by Eo, Yun-Ho Aug 30, 2024 05:49am

- When there are no changes to demand, increased supply reduces prices. This model of price determination can be applied to the pharmaceutical market. For pharmaceuticals, inducing competition between pharmaceutical companies can decrease financial expenses. However, it often results in increased time for reimbursement listing. Drug prices must be adjusted through negotiation with the government, and companies cannot adjust them arbitrarily. As we face a high-priced drug era, the government's stance is that "good things come to those who wait.' When reimbursement applications for new drugs fall into the same class, the government often discusses reimbursement listing two or even three new drugs at once when a follow-up drug approval is expected. Because drugs are high-priced, the government can use the market to its advantage by having pharmaceutical companies compete with each other. Under the National Health Insurance system, financial saving creates another opportunity. The more it saves, the more coverage the government can expand. However, the issue is the time sensitivity. In theory, it would be good to have drugs of the same class receive approval around the same time and pass reimbursement listing, but this is different in practice. The application dates of drugs that apply for reimbursement listing differ by six months to up to one year. There could be other delaying factors than the different 'application' dates. For example, among drugs with the same mechanism of action, the first-in-class drug received regular listing, whereas follow-up drugs were listed for reimbursement under the Risk Sharing Agreement (RSA). Strikingly, those drugs had been approved domestically 5-10 years ago. It is fortunate that these drugs were listed, and patients benefited. However, the process took too long. Additionally, there are differences in what pharmaceutical companies want. Companies that applied first wish to be evaluated alone. Entering the market first has the advantage in addition to drug price. Clinical data also plays a role in this issue. Even if new drugs have the same mechanism of action, their indication and clinical results may carry different weight. Indication influence reimbursement criteria, while data values affect drug prices. There is no concrete answer to this issue. We have to consider different factors. In addition to considering losses and benefits, the nature of each drug and patient circumstances must be considered. All parties must work together in order to reach an agreement embracing the Korean National Health Insurance system and pharmaceutical companies' stances.

- Company

- Korean pharma and biotechs expand R&D investments

- by Chon, Seung-Hyun Aug 29, 2024 04:32am

- Listed pharma and biotech companies have expanded their research and development (R&D) investments in Korea this year. 3 out of 5 major pharmaceutical companies increased their R&D investments from last year to discover new candidates. Pharmaceutical companies with larger sales have been more active in reinvesting in R&D. According to the Financial Supervisory Service on Monday, the R&D investment expenses of 20 major pharma and biotech companies totaled at KRW 1.236 trillion in the first half of the year, up 12.7% from KRW 1.967 trillion a year earlier. The data was compiled from the top 20 pharmaceutical companies by revenue that submitted semi-annual reports. Ildong Pharmaceutical, which spun off its R&D subsidiary last year, was not included in the survey. Thirteen of the 20 major pharmaceutical companies increased their R&D investment in the first half of the year compared to the same period last year. Celltrion, Samsung Biologics, Daewoong Pharmaceutical, Yuhan Corp, Hanmi Pharmaceuticals, Dong-A ST, SK Biopharm, HK Inno. N, Boryung Pharmaceutical, Dongkook Pharmaceutical, Huons, Dongwha Pharmaceutical, and Celltrion Pharm increased their R&D spending in the first half of the year compared to the same period last year. Celltrion invested the most, KRW 206.7 billion in R&D in the first half of the year. This is a 37.3% expansion compared to that in the first half of last year. Celltrion has completed the development of biosimilars of Remicade, Enbrel, Mabthera, and Humira and is selling them in the U.S. and Europe. Celltrion has received approval for two biosimilars in Europe this year. In May, the company received marketing authorization from the European Commission for its first biosimilar of Xolair, Omlyclo. Xolair is an antibody biopharmaceutical agent used to treat allergic asthma, chronic rhinosinusitis with nasal polyps, and chronic idiopathic urticaria. It generated global sales of about KRW 5 trillion last year. Recently, Stekima, its biosimilar version of the autoimmune disease treatment Stelara, received European marketing authorization. Stelara is an autoimmune disease treatment for plaque psoriasis, psoriatic arthritis, Crohn's disease, and ulcerative colitis developed by Janssen. Celltrion has received 8 and 6 approvals for its biosimilars in Europe and the U.S., respectively. Samsung Biologics' R&D expenditure in the first half of the year increased 20.2% year-on-year to KRW 177 billion. Samsung Biologics' main business is contract manufacturing (CMO) and contract development (CDO) of raw materials for biopharmaceuticals. Samsung Biologics' R&D organization provides technical support for the production of customer products and cell line process R&D at the Manufacturing Science And Technology (MSAT) laboratory, CDO Development Center, and Bio R&D Center. The company’s R&D investments have also increased due to the increase in orders for biopharmaceutical contract manufacturing (CMO) and contract development (CDO) orders. Samsung Biologics' R&D investment also includes Samsung Bioepis’ R&D expenses. Since 2022, Samsung Bioepis has become a wholly-owned subsidiary of Samsung Biologics. Samsung Bioepis has received a total of 4 biosimilar approvals in the U.S. and Europe this year In April, Samsung Bioepis received marketing authorization for its Stelara biosimilar Pyzchiva in Europe. In May, the company received approval for Opuviz, a biosimilar to Eylea used for macular degeneration. Following the FDA approval of Pyzchiva in June, Samsung Bioepis received marketing authorization for the rare disease treatment Epysqli in July. Epysqli is a biosimilar product of Soliris that was developed by Alexion in the US. Among traditional pharmaceutical companies, Daewoong Pharmaceutical made the largest R&D investment of KRW 111.8 billion in the first half of the year. This is an 18.3% rise year-on-year. Daewoong is developing new drugs in areas such as ulcerative colitis, idiopathic pulmonary fibrosis, obesity, autoimmune diseases, and infectious diseases. It is also conducting joint research with HanAll Biopharma, Daewoong Therapeutics, Oncocross, and D&D Pharmatech. In 2021, Daewoong Pharmaceutical received approval for its gastroesophageal reflux disease treatment Fexclu, and in 2022, it successfully commercialized Envlo, its new SGLT-2 inhibitor class diabetes drug. In the first half of the year, the company's R&D investment amounted to KRW 104.8 billion, up 20.6% year-on-year. The company's increased R&D investment was driven by the adoption of promising technologies from biotech ventures. In March, the company paid KRW 6 billion to acquire the technology of an anti-cancer drug candidate that inhibits SOS1 from Cyrus Therapeutics and Kanaph Therapeutics. In Q2, the company paid KRW 3 billion in technology fees to biotech company J Ints Bio. J Ints Bio is a biotech company that develops new anti-cancer drugs. The company has also continued to increase clinical trial expenses for its new anti-cancer drug Leclaza. The company has been conducting Phase III clinical trials on Leclaza since 2020. Until the first half of this year, the company had invested KRW 111.2 billion in Leclaza’s Phase III trial. Dong-A ST invested KRW 80.3 billion in R&D in the first half of the year, up 49.5% year-on-year. The company’s clinical expenses for new drug development increased significantly. DA-4505, its immuno-oncology drug candidate, was approved for Phase 1/2a clinical trials in Korea in November last year. DA-4505 showed improved tumor suppression through preclinical studies compared to an AhR antagonist that is being developed by a multinational pharmaceutical company. Also, the company completed its Phase III trial for DA-8010, a treatment for overactive bladder, in Korea in May. However, DA-8010 did not show a statistically significant difference. SK Biopharm, HK Inno.N, Boryung, and Celltrion Pharm increased their R&D investments by more than 10% in the first half of the year compared to the same period last year. On the other hand, R&D investments by Handok, Hugel, GC Biopharma, Jeil Pharmaceutical, Daewon Pharmaceutical, Chong Kun Dang, and JW Pharmaceutical decreased compared to the same period last year. The increase in R&D investment amongst pharmaceutical companies that posted high sales was greater. The Top 10 sales companies - Samsung Biologics, Celltrion, Yuhan Corp, Hanmi Pharmaceutical, GC Biopharma, Chong Kun Dang, Daewoong Pharmaceutical, Boryung Pharmaceutical, HK Inno.N, and Dongkook Pharmaceutical - invested KRW 938.3 billion in R&D in the first half of the year, up 13.2% year-on-year. Of the Top 10 companies by revenue, the investment volume of 8 companies other than GC Biopharma and Chong Kun Dang increased year-on-year. It is analyzed that large pharmaceutical companies with experience in developing new drugs are actively investing in R&D to discover new candidates.

- Company

- Breast cancer drug Trodelvy receives DREC deliberations

- by Eo, Yun-Ho Aug 29, 2024 04:31am

- The ADC breast cancer drug Trodelvy has made a step toward insurance reimbursement after 9 months of wait. Gilead Sciences' triple-negative breast cancer (TNBC) drug Troldelvy, whose reimbursement request received 100,000 consents in a public petition, will be presented for deliberation to the Health Insurance Review and Assessment Service's Drug Reimbursement Evaluation Committee on the 29th. The drug’s reimbursement application had remained pending for some time since its reimbursement standard was set by the Cancer Disease Review Committee in November last year. Therefore, the industry’s eye will be focused on the outcome of the committee review. The key issue will be the drug price, especially the ICER threshold value. Trodelvy is already listed in about 30 countries around the world. Trodelvy is already listed in about 30 countries around the world. Taiwan, which has a single-payer healthcare system similar to South Korea's, began reimbursing Trodelvy in February this year. The global rush to improve patient access to Trodelvy has been driven by the poor treatment environment for metastatic triple-negative breast cancer and the clinical value of Trodelvy. Triple-negative breast cancer is an aggressive form of breast cancer that recurs and metastasizes rapidly. Patients with metastatic triple-negative breast cancer who have metastasized despite treatment have a life expectancy of only a few months even with chemotherapy. However, chemotherapy has long been the standard of care due to the lack of targets that can effectively kill cancer cells. Trodelvy, the first Trop-2-targeted antibody-drug conjugate (ADC), is the only treatment for metastatic triple-negative breast cancer in the second-line or higher setting that has been shown to prolong survival compared to chemotherapy and has settled as the global standard of care since its introduction. Currently, major guidelines in the U.S. and Europe specify Troldelvy as the preferred agent for patients with previously treated metastatic triple-negative breast cancer. In a Phase III study, the overall survival of the chemotherapy arm was 6.9 months, compared to a nearly one-year survival. (11.8 months) in the Troldelvy arm, In addition, Troldelvy demonstrated an effect in controlling symptoms and pain caused by cancer and improving patients' quality of life by improving their overall health status. Trodelvy was awarded the highest possible score of 5 points on ESMO-MCBS, the European Society for Medical Oncology's (ESMO) scale used to rate the value of anticancer drugs. A score of 5 indicates that a drug is effective not only in prolonging patient survival but also in improving quality of life, and Troldelviy is the only treatment for metastatic triple-negative breast cancer to receive a score of 5 on ESMO-MCBS. In fact, the U.K. has detailed the rationale behind its assessment, stating that the state’s reimbursement decision was based on the severity of metastatic triple-negative breast cancer and the survival benefit of Troldelvy. Similar to Korea, the U.K. uses the incremental cost-effectiveness ratio (ICER) to evaluate new drugs for health insurance coverage. While the UK has one of the highest reimbursement barriers for new drugs, it applies flexible pharmacoeconomic evaluation criteria for innovative drugs used for serious conditions to improve patient access. In the UK, Troldelvy was granted preferential economic evaluation because it prolonged survival in terminally ill patients with less than 2 years life expectancy, whose population is even smaller than those of rare diseases. As a result, Trodelvy gained access with an ICER threshold that was approximately twice higher than that of general drugs. Meanwhile, Troldelvy has been the subject of a series of petitions this year, gathering more than 100,000 consents online. The Korean Alliance of Patients' Organizations also responded to the desperate pleas of patients and their caregivers when the petition was abandoned due to the expiration of the 21st National Assembly's term. In May, the organization submitted a letter directly to the Ministry of Health and Welfare requesting a prompt review of the reimbursement of drugs with high patient demand, including Trodelvy.

- Policy

- Will RWD-based reimb agreements be more beneficial?

- by Lee, Tak-Sun Aug 29, 2024 04:31am

- On the 28th, HIRA held an international symposium on Drug reimbursement contracts satisfy all parties involved when they achieve three goals: The first is patient access, the second is sustained revenue for the pharmaceutical company, and the third is budget management for the payer. “A fair price is one that can satisfy both the seller and the buyer,” said So-young Lee, Director of Health Insurance and Assessment Service’s Pharmaceutical Performance Assessment Division. ”A fair price should guarantee transparency, R&D, production costs, and innovation.” So, what kind of reimbursement agreement can satisfy all three conditions? Experts say that a reimbursement agreement based on RWD (real-world data) can be a good alternative. On the 28th, HIRA held an international symposium on 'RWD-based performance assessment of high-priced drugs' at the Ambassador Seoul Pullman Hotel in Jangchung-dong, Seoul. At the symposium, Lee delivered a keynote address on the topic of 'Sustainable access to high-cost drugs through RWD-based cooperation'. The use of the performance-based assessment system using RWD is in its infancy in Korea and other countries. In Korea, the system was first introduced in 2022 for the rare disease drug Kymriah. In order to reduce the uncertainty of drugs that received an exemption from pharmacoeconomic evaluations, the system applies post-reimbursement patient evaluation to determine whether or not to reimburse the drug. Until now, the cost-effectiveness evaluations of new drugs were determined based on clinical trial data rather than real-world patient data, but there is a global movement to use RWD data of high-priced drugs as clinical trial results do not resolve uncertainties. The UK established a real-world evidence (RWE using RWD) framework in February 2022 and has been continuing to update its guidance on valuation using RWE. “Ultra-high-priced drugs present uncertainties due to disease characteristics and ethical issues,” said Lee, adding, “ It is difficult to standardize clinical trials, and there may not be a comparator drug or enough follow-up data.” In such cases, it is difficult to analyze the cost-effectiveness, and even then, it is difficult to ensure reliability. Among the high-priced drugs listed for reimbursement in Korea, there are already 11 drugs that cost more than KRW 100 million per year. For these drugs, performance-based managed reimbursement contracts are being implemented as their pharmacoeconomic evaluation are difficult and clinical uncertainty high. To date, 5 drugs are receiving patient-level performance-based evaluations and 1 drug-level evaluation. “The industry is negative about the outcome-based drug evaluation,” Director Lee said, ”The industry believes that the system is not objectively valid or reliable.” However, Lee emphasized that RWD, if utilized well, can be used to ensure reliability and fair pricing that satisfies patients, pharmaceutical companies, and the payer. “The advantage of RWD is that evidence can be gathered from the R&D stage to benefit patients, and the incompleteness of the system can be reduced if pharmaceutical companies and the insurer can work together to link a lot of data. If we can ensure full-cycle collaboration based on transparency, the system will not shrink the pharmaceutical industry while ensuring access to good drugs for patients.” Of course, there are limitations. Data analysis needs to be done while protecting patient privacy, and transparency and uniformity of data still remain a challenge. However, standardization efforts are underway in each country. “There is still a lack of confidence in the system using RWD to evaluate cost-effectiveness, as well as limited transparency, data quality issues, and bias,” said Dr. Vandana Ayyar Gupta, Scientific Advisor of NICE in the UK, another keynote speaker at the event, ”This is why NICE is working to update its guidance and create an RWE framework for its support.” “Real-world data and real-world evidence are being used by NICE in a variety of ways, and the number of use cases is expanding,” said Dr. Gupta. ”The RWE framework will continue to be updated through communication between developers and NICE based on rapidly evolving methodologies and technological advances.”

- Opinion

- [Reporter’s View]Support domestic COVID-19 drugs

- by Lee, Hye-Kyung Aug 28, 2024 05:52am

- The recurrence of COVID-19 has sparked interest in COVID-19 drugs. After the pandemic turned into an endemic, the government set a budget of KRW 179.8 billion for COVID-19 drugs this year, which was a 53.2% cut from last year, and the number of COVID-19 drugs introduced in Q1 and Q2 of this year was 179,000, half of the 341,000 that the government procured during the same period last year. The government claimed that the budget cut was due to preparations for the reimbursement of COVID-19 treatments, but the government ultimately set aside KRW 326.8 billion in emergency reserves to purchase an additional 262,000 doses of treatment after failing to predict the resurgence of COVID-19. The amount of the reserve is nearly equivalent to the KRW 384.3 billion budget the government had set for the purchase of COVID-19 drugs last year. Due to the lack of a Korean treatment option, Korea has to rely on global pharmaceutical companies for all supplies of treatments in the event of a COVID-19 outbreak. This is because there are currently only 3 COVID-19 drugs available in Korea - Pfizer's Paxlovid Tab, MSD's Lagevrio Cap, and Gilead's Beklury Inj. If there were locally developed COVID-19 treatments, not just global pharmaceutical companies' products, the government could have addressed the outbreak faster. To stabilize the supply and demand of cold medicines, the government asks domestic pharmaceutical companies to increase production through a public-private consultative body to balance the supply and demand when medical organizations report unstable supply. The recent shortage of COVID-19 drugs is likely to have been affected by Korea’s reliance on imported products. Curing the COVID-19 pandemic, there has been a movement toward self-sufficiency of drugs. Celltrion developed Regkirona Inj and received marketing authorization in September 2021. However, in 2022, the company suspended new supplies due to its low effectiveness against omicron mutations. Following this, Ildong Pharmaceutical's Xocova, which was developed in collaboration with Japan's Shionogi Pharmaceutical, and Hyundai Bioscience's Xafty tried to cross Korea’s threshold through the emergency use authorization pathway but failed. The MFDS pointed to the small number of clinical trial subjects and requested Phase III clinical data for the domestic approval of each drug. COVID-19 treatments need to accumulate clinical data on COVID-19 patients, and this is why domestic pharmaceutical companies have been struggling to recruit patients in the endemic. The need for homegrown drugs and vaccines has been emphasized during the outbreak. The government has also provided various support such as emergency use authorization and expedited review. However, since COVID-19 was declared endemic, many people lost interest in domestic COVID-19 treatments. But the resurgence of COVID-19 this time has made everyone realize that a second or third wave could come at any time. The endemic is not the end of COVID-19. We need to expand our support for domestic drugs to ensure self-sufficiency of COVID-19 treatments in Korea.