- LOGIN

- MemberShip

- 2026-07-29 14:00:55

- Philips Korea's sales staggering…shift to service-centric

- by Hwang, byoung woo | translator Hong, Ji Yeon | 2026-04-23 10:51:06

Philips Korea’s sales growth, which had been on a recovery trend since 2023, has stalled, with growth rates remaining in the 1% range.

However, during the same period, operating profit increased significantly, showing an actual improvement in profitability. This is interpreted as the result of a shift in the sales mix, moving away from a hardware sales-centric structure toward services, including maintenance and software.

Analysis suggests that amid intensifying competition in the large-scale medical equipment market, the future growth is shifting from hardware to software and solutions.

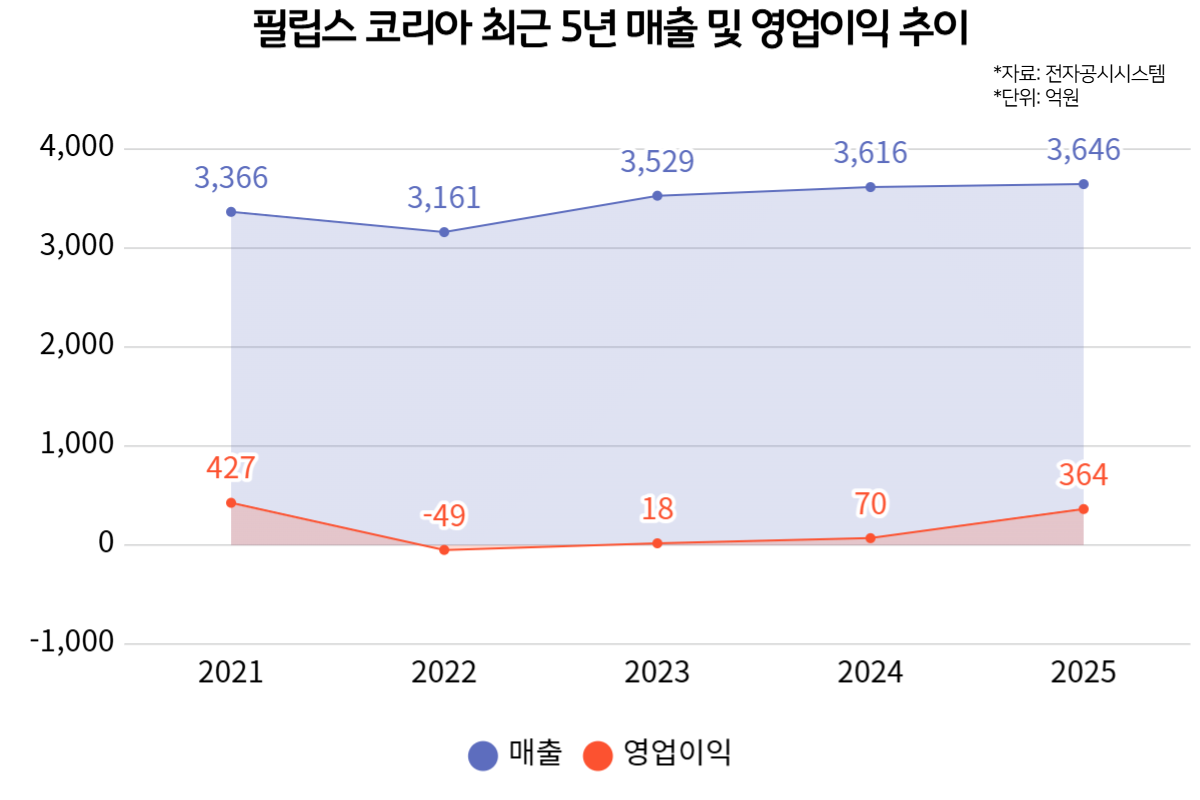

Sales Growth 'Stalls,' Operating Profit 'Rebounds

According to Philips Korea’s recently disclosed audit report, the company’s sales growth appears to have entered a period of stagnation.

Specifically, sales, which recorded KRW 336.6 billion in 2021, decreased to KRW 316.1 billion in 2022 before rebounding to KRW 352.9 billion in 2023.

Since then, however, sales reached KRW 361.6 billion in 2024 and KRW 364.6 billion in 2025, marking two consecutive years of growth limited to the 1% range following the 2023 rebound, maintaining a slowing growth.

One of the primary reasons for this sales stagnation can be traced back to the large-scale business restructuring carried out in 2021. As of September 9, 2021, Philips Korea completed the divestment of its Domestic Appliances division, which was highly profitable

This was part of Philips’ global 'Selection and Concentration' strategy to focus on the healthcare B2B (business-to-business) sector.

Considering that the Domestic Appliances division generated approximately KRW 41.8 billion in annual sales at the time, the separation of this core consumer cash cow is interpreted as a factor in the reduction of the company's overall scale.

In contrast to the slowdown in top-line growth, profitability improved significantly. Philips Korea’s operating profit shifted from KRW 42.7 billion in 2021 to a loss of KRW -4.9 billion in 2022.

After successfully returning to a surplus of KRW 1.8 billion in 2023, profit showed a recovery to KRW 7 billion in 2024, followed by KRW 36.4 billion in 2025, a more than five-fold improvement compared to the previous year.

This indicates that focusing on internal stability and reorganizing the portfolio toward high-value-added businesses, rather than external expansion, has proven effective.

Philips Diversifies the Profit Structure, Shift From Product Sales to 'Service'

The primary reasons for the improvement in operating profit are cost reductions and lower selling, general, and administrative (SG&A) expenses.

The cost of goods sold, which was KRW 270.7 billion in 2024, decreased to KRW 246.3 billion in 2025, and SG&A expenses also fell by approximately 2 billion KRW, from 83.8 billion KRW to KRW 81.8 billion. Essentially, while sales barely grew, profit rose by simultaneously reducing costs and expenses.

Furthermore, the fact that the sales structure is increasing 'service sales,' which provides maintenance and software-linked solutions in addition to equipment delivery, appears to have influenced the improvement in profitability.

Looking at Philips Korea’s sales structure by business segment (item), product sales decreased from KRW 242.9 billion in 2021 to KRW 219.6 billion in 2022, before recovering to ▲KRW 249.9 billion in 2023 and ▲KRW 254.6 billion in 2024.

However, in 2025, product sales recorded KRW 253.6 billion, showing negative growth compared to the previous year.

In contrast, service sales has been on a steady upward trajectory, with no negative growth. Service sales, which was KRW 93.7 billion in 2021, recorded KRW 96.5 billion in 2022, ▲KRW 102.9 billion in 2023 ▲KRW 106.9 billion in 2024 ▲KRW 110.9 billion in 2025.

The share of service sales in total sales also expanded from 27.8% in 2021 to approximately 30.4% in 2025.

Considering the characteristics of the Korean market, where replacement cycles for large medical equipment (MRI, CT, ultrasound, etc.) are long and large-scale orders following the establishment of new hospitals are limited, the expansion of service-oriented sales, such as software upgrades and Service Level Agreements (SLA) for pre-installed equipment, is analyzed to have played a key role in defending profitability.

Intensifying Imaging Competition… The Challenge of Growth Drivers

Because of this, Philips Korea is also seeking a breakthrough by creating a digital healthcare environment centered on artificial intelligence (AI) technology.

As global competitors such as Siemens Healthineers and GE HealthCare integrate AI solutions with hardware, Philips is moving to capture the early market.

For example, Philips Korea is establishing smart hospital collaborations focused on AI-based improvements to ultrasound and imaging workflows.

With the recent domestic medical environment emphasizing smart hospitals amid personnel shortages, Philips appears focused on embedding its portfolio, spanning diagnostic imaging·ultrasound·interventional procedure systems, into these systems.

However, expanding the influence of diagnostic imaging equipment, which is the most fundamental driver of external growth, remains a challenge.

In this context, Philips' next-generation spectral CT, the Verida system, which recently received U.S. Food and Drug Administration (FDA) clearance, could potentially provide a way forward.

The core of Verida system is its spectral technology. While most CT scanners focus on providing structural information by imaging the human body at a single energy, spectral CT analyzes differences in tissue composition across multiple energy spectra.

As it promotes clinical efficiency improvement rather than just simple image quality enhancement, there is potential for synergy with future smart hospital system construction.

An official from the medical device industry stated, "While Philips Korea's new products and technological innovations, such as helium-free MRI and cardiac ultrasound, are receiving positive responses, hospital investment decisions are made on a mid-to-long-term basis due to the nature of the market," and added, "The impact of new products is more likely to be reflected in mid-to-long-term trends rather than short-term performance."

-

- 0

댓글 운영방식은

댓글은 실명게재와 익명게재 방식이 있으며, 실명은 이름과 아이디가 노출됩니다. 익명은 필명으로 등록 가능하며, 대댓글은 익명으로 등록 가능합니다.

댓글 노출방식은

댓글 명예자문위원(팜-코니언-필기모양 아이콘)으로 위촉된 데일리팜 회원의 댓글은 ‘게시판형 보기’와 ’펼쳐보기형’ 리스트에서 항상 최상단에 노출됩니다. 새로운 댓글을 올리는 일반회원은 ‘게시판형’과 ‘펼쳐보기형’ 모두 팜코니언 회원이 쓴 댓글의 하단에 실시간 노출됩니다.

댓글의 삭제 기준은

다음의 경우 사전 통보없이 삭제하고 아이디 이용정지 또는 영구 가입제한이 될 수도 있습니다.

-

저작권·인격권 등 타인의 권리를 침해하는 경우

상용 프로그램의 등록과 게재, 배포를 안내하는 게시물

타인 또는 제3자의 저작권 및 기타 권리를 침해한 내용을 담은 게시물

-

근거 없는 비방·명예를 훼손하는 게시물

특정 이용자 및 개인에 대한 인신 공격적인 내용의 글 및 직접적인 욕설이 사용된 경우

특정 지역 및 종교간의 감정대립을 조장하는 내용

사실 확인이 안된 소문을 유포 시키는 경우

욕설과 비어, 속어를 담은 내용

정당법 및 공직선거법, 관계 법령에 저촉되는 경우(선관위 요청 시 즉시 삭제)

특정 지역이나 단체를 비하하는 경우

특정인의 명예를 훼손하여 해당인이 삭제를 요청하는 경우

특정인의 개인정보(주민등록번호, 전화, 상세주소 등)를 무단으로 게시하는 경우

타인의 ID 혹은 닉네임을 도용하는 경우

-

게시판 특성상 제한되는 내용

서비스 주제와 맞지 않는 내용의 글을 게재한 경우

동일 내용의 연속 게재 및 여러 기사에 중복 게재한 경우

부분적으로 변경하여 반복 게재하는 경우도 포함

제목과 관련 없는 내용의 게시물, 제목과 본문이 무관한 경우

돈벌기 및 직·간접 상업적 목적의 내용이 포함된 게시물

게시물 읽기 유도 등을 위해 내용과 무관한 제목을 사용한 경우

-

수사기관 등의 공식적인 요청이 있는 경우

-

기타사항

각 서비스의 필요성에 따라 미리 공지한 경우

기타 법률에 저촉되는 정보 게재를 목적으로 할 경우

기타 원만한 운영을 위해 운영자가 필요하다고 판단되는 내용

-

사실 관계 확인 후 삭제

저작권자로부터 허락받지 않은 내용을 무단 게재, 복제, 배포하는 경우

타인의 초상권을 침해하거나 개인정보를 유출하는 경우

당사에 제공한 이용자의 정보가 허위인 경우 (타인의 ID, 비밀번호 도용 등)

※이상의 내용중 일부 사항에 적용될 경우 이용약관 및 관련 법률에 의해 제재를 받으실 수도 있으며, 민·형사상 처벌을 받을 수도 있습니다.

※위에 명시되지 않은 내용이더라도 불법적인 내용으로 판단되거나 데일리팜 서비스에 바람직하지 않다고 판단되는 경우는 선 조치 이후 본 관리 기준을 수정 공시하겠습니다.

※기타 문의 사항은 데일리팜 운영자에게 연락주십시오. 메일 주소는 dailypharm@dailypharm.com입니다.

- “Drug pricing intervention contributes to the crisis in essential healthcare and shortage of drugs”

- Reporter's view | Lee, Jeong-Hwan